Construction project insurance safety requirements define the mandatory coverage policies, endorsement structures, and safety protocols that contractors, project managers, and developers must maintain to protect their workforce, assets, and legal standing throughout the project lifecycle. The industry standard term for this integrated framework is construction risk management. Getting it right means combining the correct insurance policies with active, documented safety controls. Miss either element and you expose your project to uncapped financial liability. This guide covers the specific coverages required by law, the endorsements most frequently missing from certificates, and the safety protocols that directly affect your premiums and claim acceptance.

What essential insurance coverages are legally required for construction projects?

Construction remains one of the highest-hazard sectors in the economy, recording 9.6 fatal injuries per 100,000 full-time equivalent workers. That fatality rate is the primary driver behind statutory insurance mandates at both federal and state levels.

Workers’ Compensation is required in 49 states. Premiums typically run from $5 to $30 per $100 of payroll, depending on trade classification and claims history. This coverage pays medical costs and lost wages for injured workers regardless of fault, which removes the most common source of catastrophic project liability.

Commercial General Liability (CGL) insurance sets the floor for third-party bodily injury and property damage claims. Minimum limits for most residential contracts are $1 million per occurrence and $2 million aggregate. Commercial projects routinely require $2 million per occurrence and $4 million aggregate. These thresholds are not suggestions. They appear verbatim in most owner-contractor agreements and subcontract templates.

Builders Risk insurance covers work in progress against theft, fire, vandalism, and weather events. Builders Risk is priced at roughly 1–3% of total contract value. A $10 million project therefore carries a Builders Risk premium in the range of $100,000 to $300,000 annually. That cost is almost always passed through to the project budget.

Umbrella and Excess Liability policies sit above the CGL and auto liability limits. Serious injuries can exceed CGL limits within hours of a major incident. An umbrella policy provides the critical buffer that prevents a single claim from wiping out a contractor’s balance sheet.

For public works contracts, the Miller Act requires surety bonds on federal projects exceeding $150,000. Many state and municipal contracts mirror this threshold. Bonds are not insurance. They guarantee contract performance and payment to subcontractors and suppliers.

| Coverage Type | Typical Minimum | Trigger |

|---|---|---|

| Workers’ Compensation | Statutory (49 states) | Employee injury or illness |

| Commercial General Liability | $1M/$2M (residential); $2M/$4M (commercial) | Third-party bodily injury or property damage |

| Builders Risk | 1–3% of contract value | Physical loss to work in progress |

| Umbrella/Excess Liability | $1M–$5M above primary | Claims exceeding primary policy limits |

| Surety Bond | Per contract value | Non-performance or non-payment |

Pro Tip: Always confirm that your Builders Risk policy includes “soft costs” coverage for architect fees, permit re-application costs, and loan interest incurred during a rebuild delay. Most standard forms exclude these by default.

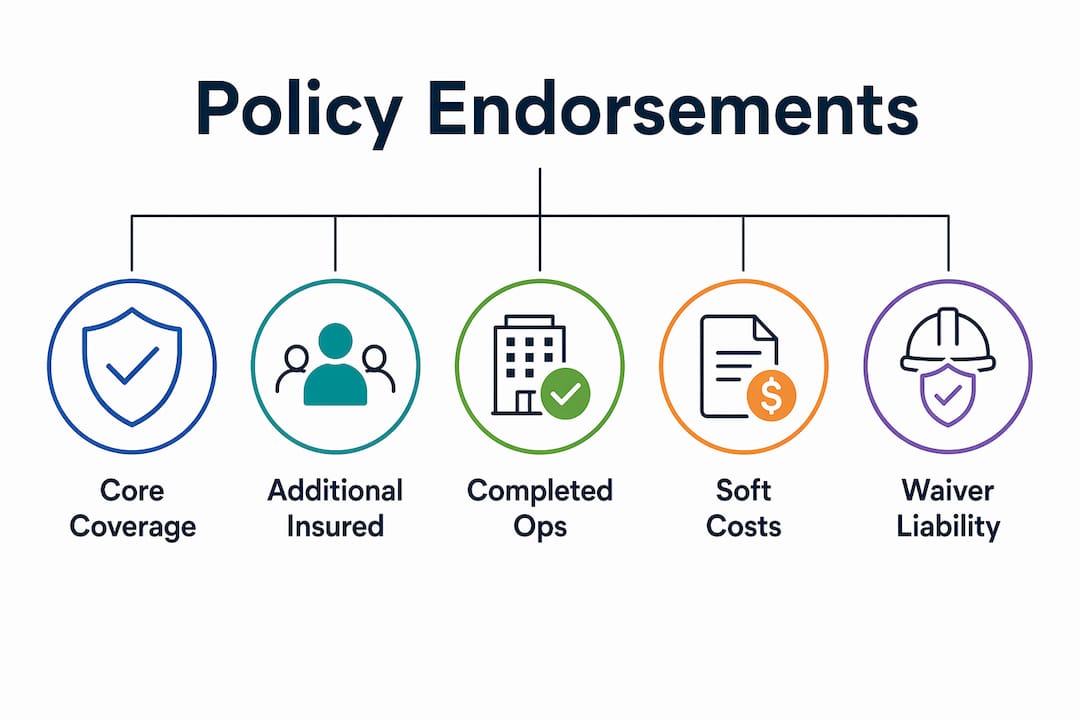

Which policy endorsements are indispensable for full stakeholder protection?

Buying the right policies is necessary but not sufficient. The endorsements attached to those policies determine whether coverage actually responds when a claim is filed. Project managers who skip this verification step discover the gaps at the worst possible moment.

The Additional Insured endorsement CG 20 10 extends your CGL policy to cover the project owner and general contractor for claims arising from your ongoing operations. Most commercial contracts require this endorsement by name before mobilization is permitted. A certificate of insurance that lists the owner as an additional insured without the CG 20 10 form attached is legally unenforceable.

The CG 20 37 Completed Operations endorsement is the most frequently missing and most dangerous coverage gap in construction. Claims for structural defects appear years after completion, long after the project has been closed out. Without CG 20 37, a subcontractor’s policy provides zero coverage for those latent defect claims. The general contractor and owner are left exposed.

Two additional provisions appear in virtually every major commercial contract:

- Waiver of Subrogation: Prevents your insurer from suing another party on the project after paying your claim. Without it, your insurer can pursue the owner or another contractor, creating adversarial relationships mid-project.

- Primary and Non-Contributory: Requires your policy to respond first before any other coverage the additional insured carries. Without this provision, insurers argue over which policy pays, delaying claim resolution.

Certificate of Insurance rejections most commonly occur because endorsements were not bound before the COI was issued. An insurance agent can print a certificate showing any endorsement, but if the endorsement has not been formally added to the policy, it does not exist. Verify the actual policy documents, not just the certificate.

Pro Tip: Request a copy of the actual endorsement forms, not just the ACORD certificate. The ACORD 25 form has no legal standing on its own. The bound endorsement is the only document that creates coverage.

How to integrate safety protocols with insurance compliance and construction risk management

Active safety management and insurance compliance are not parallel tracks. They are the same track. Insurance alone is ineffective without integrated safety management and subcontractor oversight. This is the core principle of enterprise-level construction risk management.

OSHA mandates a written emergency action plan on every covered construction site. Beyond that statutory baseline, OSHA compliance requires daily walk-downs by supervisors, weekly formal inspections, and monthly safety audits. Each of these activities must be documented. Documentation is what transforms a safety program from a policy statement into evidence of reasonable care.

The “Fatal Four” hazards identified by OSHA account for nearly 60% of construction fatalities: falls, struck-by incidents, electrocution, and caught-in or caught-between events. Each of these hazards generates both OSHA citations and insurance claims. A single fall fatality can trigger a workers’ compensation claim, a CGL claim, and an OSHA fine simultaneously.

The Experience Modification Rate (EMR) is the mechanism that connects your safety record directly to your insurance premiums. EMR is calculated after three years of payroll and claims history. A clean claims record leads to premium discounts, while a poor safety record can produce surcharges of up to 20%. An EMR above 1.0 also disqualifies many contractors from bidding on public and institutional projects.

- Implement daily Safe Start Checks before each task begins. Safe Start Checks shift safety culture from reactive to preventive, reducing incident frequency and the associated insurance costs.

- Assign supervisor accountability for fall protection compliance on every shift. Falls are the leading source of both OSHA citations and workers’ compensation claims.

- Conduct weekly formal site inspections and record findings in a dated log. This log is the primary evidence insurers review when evaluating claim legitimacy.

- Complete monthly safety audits covering all active subcontractors. Audit findings must be closed with documented corrective actions, not just noted.

- Maintain a project-specific safety plan that references the construction risk mitigation guide applicable to your site conditions and trade mix.

“Short, actionable risk plans with defined tolerance thresholds ensure risk management remains a routine operational rhythm rather than an occasional static document.” — Construction Risk Management for Predictable Delivery

Pro Tip: Tie supervisor performance reviews to safety audit scores. When site leaders know their EMR impact is tracked at the individual level, safety walk-down compliance rates increase measurably.

What are the best practices for verifying insurance and maintaining project compliance?

Verification is where most compliance programs fail. Project managers collect certificates at onboarding and then never check them again. Policies expire mid-project. Endorsements get dropped at renewal. Subcontractors swap out their coverage without notifying the general contractor.

The Certificate of Insurance (COI) verification process must include four specific checks: confirm policy effective and expiration dates against the project schedule, verify that the named insured matches the contracting entity exactly, confirm that all required endorsements are listed by form number, and check that coverage limits meet the project-specific minimums, not just the contractor’s standard company-level limits.

Many contractors rely on company-level insurance regardless of project-specific requirements. Generic certificates routinely miss the coverage minimums and endorsements that a specific contract demands. The fix is straightforward: require every subcontractor to provide a project-specific certificate that references the contract by name and number.

Subcontractor onboarding documentation must include more than a COI. A complete onboarding package covers:

- Current OSHA 10 or OSHA 30 cards for all supervisors

- Site-specific safety orientation acknowledgment signed by each worker

- Proof of project-specific insurance with all required endorsements bound

- Training records for any specialized work (confined space, scaffolding, crane operations)

- A completed subcontractor safety onboarding checklist reviewed and approved before first day on site

Weekly risk review rhythms with documented closure evidence prevent hazards from remaining unresolved across multiple work cycles. A hazard is not closed until the corrective action is verified in the field and recorded in writing. This standard protects both the project and the insurance claim record.

| Verification Task | Frequency | Responsible Party |

|---|---|---|

| COI expiration date check | Monthly | Project manager |

| Endorsement form number verification | At onboarding and renewal | Contract administrator |

| Subcontractor safety document review | At onboarding | Site safety officer |

| OSHA training record audit | Quarterly | Safety manager |

| Risk register review and closure | Weekly | Project manager |

Pro Tip: Set calendar reminders 60 days before each subcontractor’s policy expiration date. Replacing a non-compliant contractor mid-project costs far more in schedule delay than the time spent on proactive renewal tracking.

Key Takeaways

Effective construction project insurance safety requirements demand verified policy endorsements, project-specific coverage minimums, and active safety documentation working together as a single compliance system.

| Point | Details |

|---|---|

| Mandatory coverage baseline | Workers’ Compensation, CGL, Builders Risk, and Umbrella policies are the statutory and contractual minimum for most projects. |

| Endorsements determine real coverage | CG 20 10 and CG 20 37 must be bound before COI issuance or coverage does not legally exist. |

| Safety record drives premium cost | EMR surcharges up to 20% apply for poor safety records; clean claims history produces measurable discounts. |

| Project-specific certificates required | Generic company-level COIs routinely miss contract-specific minimums and endorsements. |

| Weekly verification prevents gaps | Risk registers and COI expiration tracking must run on a weekly rhythm with documented closure evidence. |

The compliance gap no one talks about

The most common failure I see in construction insurance compliance is not a missing policy. It is a missing conversation. Project managers buy the right coverages, collect the certificates, and then treat the file as closed. The endorsements were never verified against the actual policy. The subcontractor’s agent issued a certificate that reflected what the contract required, not what was actually bound.

I have reviewed projects where the CG 20 37 Completed Operations endorsement was listed on every COI in the file and absent from every actual policy. The general contractor had no idea until a structural defect claim arrived three years after handover. At that point, the subcontractors’ policies provided zero coverage, and the general contractor’s own CGL became the only line of defense.

The second failure is treating safety protocols as a compliance checkbox rather than a premium management tool. An EMR above 1.0 does not just raise your premiums. It removes you from bidding pools on the projects that matter most. The contractors who maintain EMRs below 0.8 consistently do so because their site leaders treat daily walk-downs and Safe Start Checks as non-negotiable operational standards, not paperwork exercises.

My recommendation is direct: assign one person on every project the explicit responsibility of verifying endorsement forms against actual policy documents at onboarding and at every renewal. Pair that with a risk assessment process that runs on a weekly rhythm. Those two practices eliminate the majority of coverage gaps and compliance failures before they become claims.

— Aman

How Com supports construction insurance compliance and safety management

Construction teams that need structured support for insurance compliance and safety program development work with Com, the consultancy practice behind MOSAIC Ecoconstruction Solutions. Com delivers compliance audits, safety program development, and risk assessment services specifically calibrated for construction project requirements.

Com’s consultants verify that your site safety protocols align with OSHA requirements, that your subcontractor documentation meets project-specific insurance minimums, and that your safety culture supports the EMR performance your business needs. For teams pursuing formal certification, Com provides BizSAFE Star certification support that builds insurance readiness alongside regulatory compliance. Contact Com through mosaicsafety.com.sg to discuss your project’s specific compliance requirements.

FAQ

What insurance is legally required for construction projects?

Workers’ Compensation is required in 49 states, and most commercial contracts mandate Commercial General Liability insurance at minimum limits of $1 million per occurrence and $2 million aggregate. Builders Risk and surety bonds are required by contract or statute depending on project type and value.

What is the CG 20 37 endorsement and why does it matter?

CG 20 37 is the Completed Operations endorsement that extends CGL coverage to claims arising after project completion, including structural defect claims that appear years after handover. Without it, a subcontractor’s policy provides no coverage for post-completion liability.

How does the Experience Modification Rate affect insurance premiums?

The EMR is calculated from three years of payroll and claims history and directly adjusts your Workers’ Compensation premium up or down. Poor safety records can produce surcharges of up to 20%, while a clean claims history generates discounts.

What should a subcontractor insurance verification checklist include?

A complete verification checklist confirms policy expiration dates, named insured accuracy, project-specific coverage limits, and the presence of CG 20 10 and CG 20 37 endorsements by form number, all verified against the actual bound policy documents rather than the ACORD certificate alone.

How often should construction teams review their risk and compliance documentation?

Risk registers should be reviewed weekly with documented closure evidence for each open hazard item. COI expiration dates require monthly checks, and subcontractor training records should be audited quarterly to maintain continuous project insurance compliance.